Latest Trends in China’s ESG Reporting Policies and Regulations

Latest Trends in China’s ESG Reporting Policies and RegulationsESG stands for Environmental, Social, and Governance. Its core philosophy encourages companies to integrate these three factors into their corporate development strategies while encouraging investors to incorporate them into investment decision-making.

In China, the term “ESG Report” is often used interchangeably with “Sustainability Report.” Under current regulatory requirements, reports disclosed by listed companies should be titled “Sustainability Report” or “Environmental, Social, and Governance Report,” collectively referred to as Sustainability Reports.

China’s ESG disclosure system has evolved from spontaneous market exploration to unified regulatory standardization. In the early stages, reporting primarily took the form of Corporate Social Responsibility (CSR) reports, with disclosure encouraged rather than mandated. Standards were fragmented, lacking a unified basis for preparation, and quality was inconsistent—often favoring qualitative descriptions over quantitative data. Since 2024, driven by new policies, China’s ESG sector has entered a period of rapid acceleration characterized by:

- Systematization: The Ministry of Finance and nine other ministries released the Basic Standards for Corporate Sustainability Disclosure (Trial), establishing a unified national top-level standard that aligns with International Sustainability Standards Board (ISSB) standards.

- Legalization: The CSRC revised the Administrative Measures for Information Disclosure by Listed Companies, incorporating sustainability reports into the statutory disclosure system for the first time at the departmental regulation level. This marks the transition of A-share ESG disclosure from “voluntary guidance” to “statutory mandatory.”

- Practicality: The Shanghai, Shenzhen, and Beijing Stock Exchanges released the Guidelines for the Preparation of Sustainability Reports for Listed Companies, creating a “Mandatory Guidelines + Practical Guide” system to help enterprises overcome difficulties in report preparation.

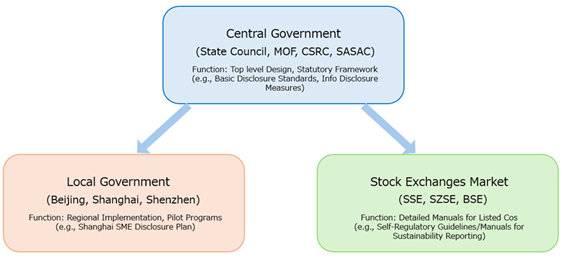

1. Major Policy Developments Since 2024

Between 2024 and 2025, a series of critical ESG policies were released by central and local governments and major exchanges, building a sustainability disclosure system with Chinese characteristics.

China ESG Policy/ Regulation Framework

China ESG Policy/ Regulation Framework

Table 1: Key ESG Policies/Regulations Since 2024

| Category | Policy Name | Date | Issuing Authority | Summary |

|---|---|---|---|---|

| Central Government | Self-Regulatory Guidelines for Listed Companies — Sustainability Reports (Trial) | April 2024 | SSE, SZSE, BSE | Unified the first A-share mandatory ESG disclosure framework. |

| Guiding Opinions on High-Standard Social Responsibility Fulfillment by Central Enterprises | June 2024 | SASAC | Promotes a shift from “disclosure presence” to “disclosure quality” for state-owned enterprises. | |

| Basic Standards for Corporate Sustainability Disclosure (Trial) | Nov 2024 | Ministry of Finance & 9 Ministries | National top-level framework aligned with ISSB standards. | |

| Administrative Measures for Information Disclosure by Listed Companies | Mar 26, 2025 | CSRC | Establishes the statutory status of sustainability reports within the regulatory system. | |

| Code of Corporate Governance for Listed Companies (Revised) | Oct 2025 | CSRC | Clarifies ESG disclosure responsibilities at the governance level. | |

| Corporate Sustainability Disclosure Standard No. 1 — Climate (Trial) | Dec 2025 | MOF, MEE | First specific standard detailing climate governance, risks, and GHG emissions. | |

| Local Government | Action Plan for Promoting High-Quality Development of ESG System in Beijing | June 2024 | Beijing Municipal DRC | First provincial-level ESG system plan to support green development. |

| Implementation Plan for Environmental Information Disclosure by SMEs in Shanghai (Trial) | Dec 2024 | PBOC Shanghai, etc. | Promotes environmental disclosure for SMEs via a green finance platform. | |

| Work Plan for Promoting the ESG System in Shenzhen (2025–2027) | Mar 2025 | Shenzhen Municipal DRC | Aims for full ESG disclosure coverage by municipal state-owned enterprises. | |

| Stock Exchange Guidelines | Self-Regulatory Guidelines/Manuals for Sustainability Reporting (SSE No. 14 / SZSE No. 17 / BSE No. 11) | April 2024 / Jan 2025 / Jan 2026 | SSE, SZSE, BSE | Established mandatory rules, refined frameworks, and provided practical examples. |

2. Analysis of Key Policies

2.1 Basic Standards (Trial): The National Top-Level Standard

Released in November 2024, this established the first unified national standard for corporate sustainability disclosure.

- Core Content: Defines objectives, principles, and information quality requirements based on four pillars: Governance — Strategy — Risk and Opportunity Management — Metrics and Targets.

- Strategy: Adopts a “priority-based, pilot-first, and gradual” approach. It aims to release climate disclosure standards by 2027 and complete the national unified system by 2030.

2.2 CSRC Administrative Measures (2025 Revision): Statutory Status

This revision moved ESG reporting from a “best practice” to a legal requirement for A-share companies.

- Article 65: Explicitly states that listed companies shall publish sustainability reports in accordance with stock exchange rules.

- Liability: Incorporates non-disclosure or false disclosure of ESG data into the scope of securities regulatory accountability.

2.3 Exchange Guidelines and Manuals: Mandatory Rules for A-Shares

Synchronized in April 2024, these guidelines identified the first batch of mandatory disclosers for the 2024 reporting year.

- Mandatory Entities: Includes companies in the SSE 180, STAR 50, SZSE 100, and ChiNext Index, as well as dual-listed (domestic and overseas) companies (covering ~450 firms).

- Scope: Identifies 21 material topics across E, S, and G dimensions.

- 2026 Update: Added specific application guides for pollutant emissions, energy utilization, and water resource utilization.

3. Corporate Response and Current Status

- Listed Companies

As of June 30, 2025, 2,481 A-share companies disclosed 2024 sustainability reports (a 46.09% disclosure rate). The financial industry leads with a 91.94% disclosure rate. - State-Owned Enterprises (SOEs)

As of July 2025, all 379 central-enterprise-controlled listed companies achieved 100% ESG report coverage. - SMEs

Shanghai and Shenzhen are leading the way in extending requirements to SMEs through pilot programs and digital accounting tools. - Quality

Quantitative disclosure has become mainstream. Nearly two-thirds of companies now disclose GHG emissions. Third-party assurance is also on the rise, with 226 A-share companies seeking external verification in 2024.

4. Outlook and Future Trends

As China enters the “15th Five-Year Plan” period, ESG reporting will trend toward:

- Expansion from Large to Small Entities: Mandatory disclosure will gradually extend from core index companies to all listed firms and eventually SMEs, following the “pilot-first, gradual” strategy.

- From “Compliance-Oriented” to “Quality-Oriented”: Policies are shifting toward the “actions speak louder than words” principle. ESG performance is increasingly being linked to executive compensation in SOEs.

- Refinement of Disclosures: With the 2026 addition of specific guides for pollutants, energy, and water, reporting is becoming more granular and operational rather than just theoretical.

- Standardization of ESG Evaluation: The implementation of the first national ESG standard for bond issuers (GB/T 46912-2025) in April 2026 marks the beginning of using ESG data for credit and value assessment.